Introduction

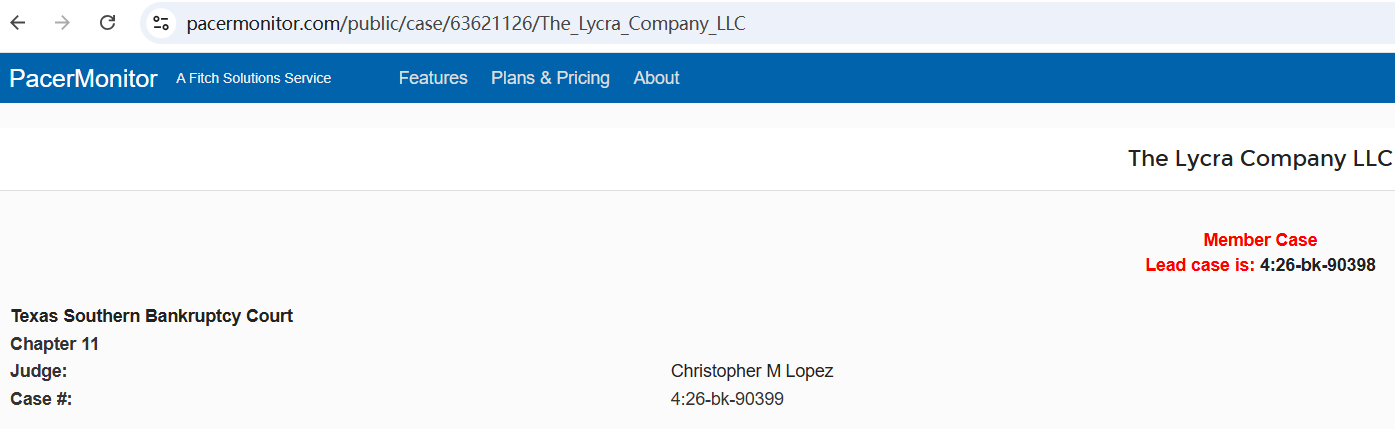

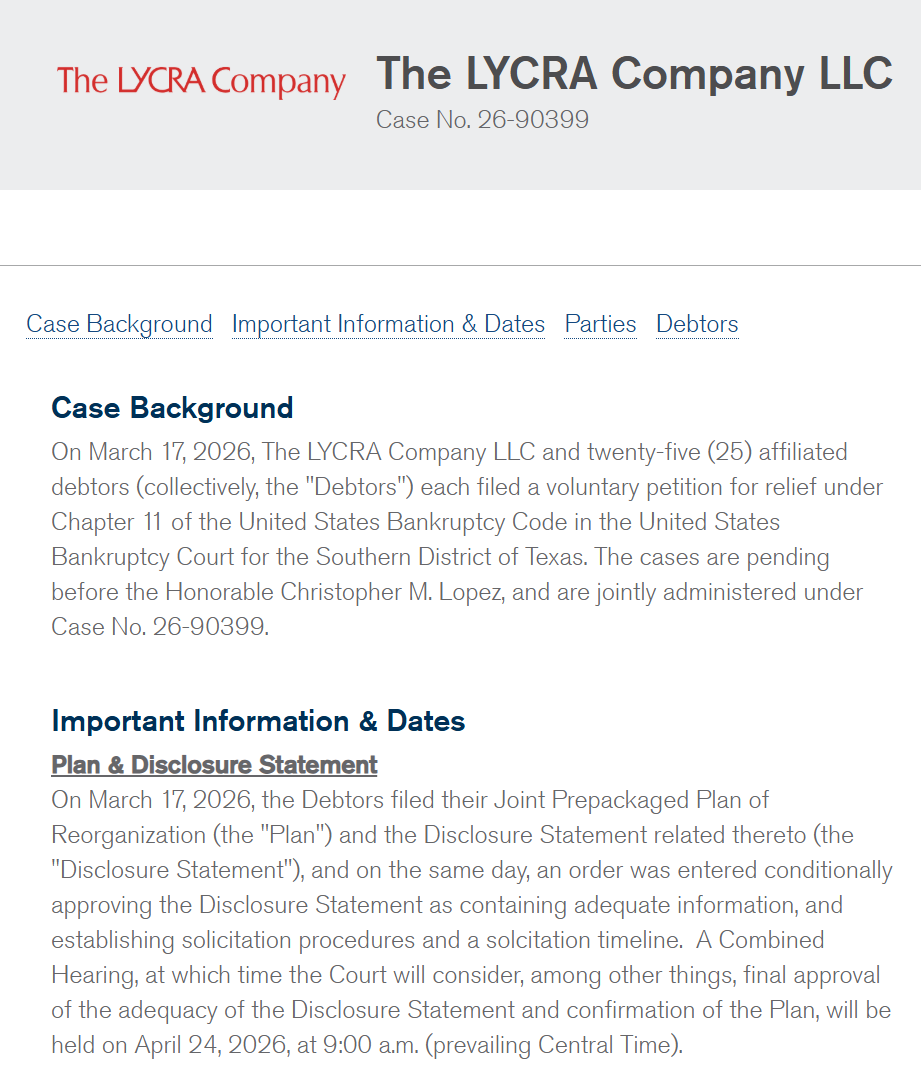

Lycra, the global spandex giant with a 68-year history, officially filed for Chapter 11 bankruptcy protection on March 17, 2026, in the U.S. Bankruptcy Court for the Southern District of Texas (Case No. 4:26-bk-90399). The cases are pending before the Honorable Christopher M. Lopez, and are jointly administered under Case No. 26-90399.

A list of those entities included in the filing can be found at restructuring.ra.kroll.com/lycra.

This brand, which once defined global standards for elastic fibers and dominated the Chinese market for decades, has come to a dramatic end. This is far from being a simple case of corporate failure—it is a concentrated reflection of the broader survival challenges faced by foreign-invested chemical fiber enterprises in China.

From Market Dominance to Decline

From an industry observer’s perspective, Lycra’s rise and fall clearly reveals the disruptive transformation of China’s chemical fiber industry, as well as the collective confusion and struggle of foreign companies amid the rise of domestic competitors and rapidly changing market conditions. This article analyzes the underlying logic behind this phenomenon through industry trends and data.

Looking back to the 1990s, foreign chemical fiber companies represented by Lycra held an absolute dominant position when they first entered the Chinese market. At that time, China’s chemical fiber industry was still in its early stages. High-end elastic fibers and specialty chemical fibers relied almost entirely on imports.

Leveraging DuPont’s technological backing, superior product performance, and an innovative “fiber + branded hangtag” model, Lycra quickly monopolized the high-end fabric market in China. Its products commanded a premium of 40%–60% over domestic fibers and became a standard component of premium textile products.

During the same period, companies such as Invista, Toray, and Hyosung controlled pricing power in the high-end chemical fiber sector through core patents, advanced equipment, and strong branding, creating substantial technological barriers. Meanwhile, domestic companies were concentrated in the low- to mid-end segments, unable to compete in technology, capacity, or brand strength.

China became a key growth engine for foreign enterprises. For Lycra alone, 29% of its revenue in fiscal year 2025 came from China, highlighting the significant industry dividends at the time.

Why Did Lycra Fail?

However, this advantage did not last long. Lycra’s decline had long been foreshadowed and reflects common structural issues faced by foreign chemical fiber companies in China. The core challenges can be summarized into three main aspects:

1. Collapse of Technological Advantage and Irreversible Domestic Substitution

The core competitiveness of foreign companies once relied on technological monopoly. However, after years of intensive R&D, Chinese domestic chemical fiber companies have achieved leapfrog development.

In the spandex sector, leading domestic companies such as Huafon Chemical(华峰化学) and Taihe New Materials(泰和新材) have broken through key production technologies. Their products now match or even surpass foreign brands in certain performance indicators.

By 2025, China accounted for nearly 80% of global effective spandex production capacity, forming a strong scale advantage. Domestic fibers, with their high cost-performance ratio, have continuously eroded the premium of foreign products. Lycra’s premium dropped from over 40% to around 10%, and in off-seasons, it even had to lower prices to secure orders, leading to a sharp decline in gross margins.

Other foreign companies like Hyosung and Taekwang have also been heavily impacted. Taekwang has suffered continuous losses in China, while Hyosung plans to shut down its domestic factories. The technological moat of foreign enterprises has been completely breached.

2. Strategic Rigidity and Lack of Localization

Lycra underwent multiple ownership changes, and management instability led to a shift in focus from long-term R&D to short-term profit extraction. R&D investment dropped sharply from over 5% during the DuPont era to less than 1%, resulting in a complete stagnation of core technology upgrades.

At the same time, the company continued to apply a unified global strategy, ignoring China’s fast-evolving and highly customized market demands. As local brands rose and trends such as green textiles and customized fabrics gained traction, Lycra failed to adjust its product structure in time.

Instead, it loosened control over its hangtag authorization system, overextending its brand value and eventually losing market trust.

This is not an isolated case. Many foreign chemical fiber companies in China adhere to rigid headquarters-driven management models, with slow decision-making and delayed responses to market changes. They continue to rely on a “premium pricing” mindset, unwilling to increase investment in local R&D and production, resulting in a growing disconnect between products and market demand.

3. High Costs and Intensified Competition

Global inflation, along with rising energy and raw material costs, has further squeezed profit margins for foreign enterprises. Lycra’s factories saw capacity utilization drop to around 60%, with profits insufficient to cover debt interest, ultimately leading to bankruptcy restructuring.

Foreign companies in China generally face higher operating costs, including overseas management expenses, maintenance of aging equipment, and stricter environmental compliance costs. Meanwhile, domestic competitors offer lower prices and higher efficiency, pushing product prices close to cost levels and leaving extremely limited profit margins.

In addition, uncertainties in the global trade environment and geopolitical factors have disrupted supply chains, increasing operational risks and making survival even more challenging for foreign companies in China.

Current Survival Landscape

Today, foreign chemical fiber enterprises in China have diverged into three distinct paths:

1. Exit or Contraction:

Companies like Lycra and Taekwang are gradually reducing capacity or withdrawing from the Chinese market due to declining competitiveness and high costs.

2. Niche Specialization:

Companies like Toray and Asahi Kasei focus on high-end specialty fibers and advanced composite materials where domestic players have not yet fully caught up.

3. Deep Localization:

A small number of companies are attempting to integrate into China’s industrial ecosystem by establishing joint R&D centers and sharing channels and production capacity with local partners.

Conclusion

Lycra’s downfall serves as a wake-up call for the entire foreign-invested chemical fiber industry in China.

The era of easy profits for foreign companies is over. Chinese domestic enterprises have built a complete industrial chain from low-end to high-end, with more intense competition, faster technological iteration, and more dynamic market demand.

To sustain development in China, foreign companies must abandon outdated mindsets and fully embrace localization—embedding R&D, production, and marketing within the domestic market and responding quickly to downstream brand needs.

At the same time, they must move beyond a single premium-pricing strategy, refocus on innovation in areas such as sustainability and functional fibers, and actively collaborate with domestic enterprises to achieve complementary advantages and integrate into China’s industrial ecosystem.

China's chemical fiber market still holds enormous potential. However, only those foreign companies that adapt to market changes, shed arrogance, and proactively transform will be able to secure a stable position in the ongoing industry reshuffle.

The era of Lycra has come to an end. It also marks the beginning of a new phase of transformation for foreign chemical fiber enterprises in China—one that requires alignment with industry trends to achieve long-term survival and growth.